Understanding the AI J-Curve

Navigating Short-Term Disruption for Long-Term Transformation.

Understanding the AI J-Curve

1. Executive Summary

Artificial intelligence promises to revolutionize business operations, yet organizations worldwide are experiencing a paradoxical reality: AI adoption often leads to initial productivity losses before delivering substantial gains. This phenomenon, known as the AI J-curve, reveals that the path to AI-driven transformation is neither linear nor immediate. As we enter 2026, understanding this trajectory has become critical for business leaders navigating the gap between AI's transformative potential and its current measurable impact.

Key Implications for Leaders:

- Expect a productivity dip: Plan for a 1-2 year adjustment period where performance may temporarily decline as organizations invest in data infrastructure, workforce training, and process redesign.

- Prioritize data and analytics foundations: 70% of companies rate analytical thinking as essential; robust data platforms and governance accelerate movement through the J-curve.

- Treat AI as organizational transformation: Technology deployment alone fails without complementary investments in operating models, workflows, and change management.

- Focus on augmentation first: AI augmenting human capabilities delivers faster wins and reduces organizational resistance compared to wholesale automation approaches.

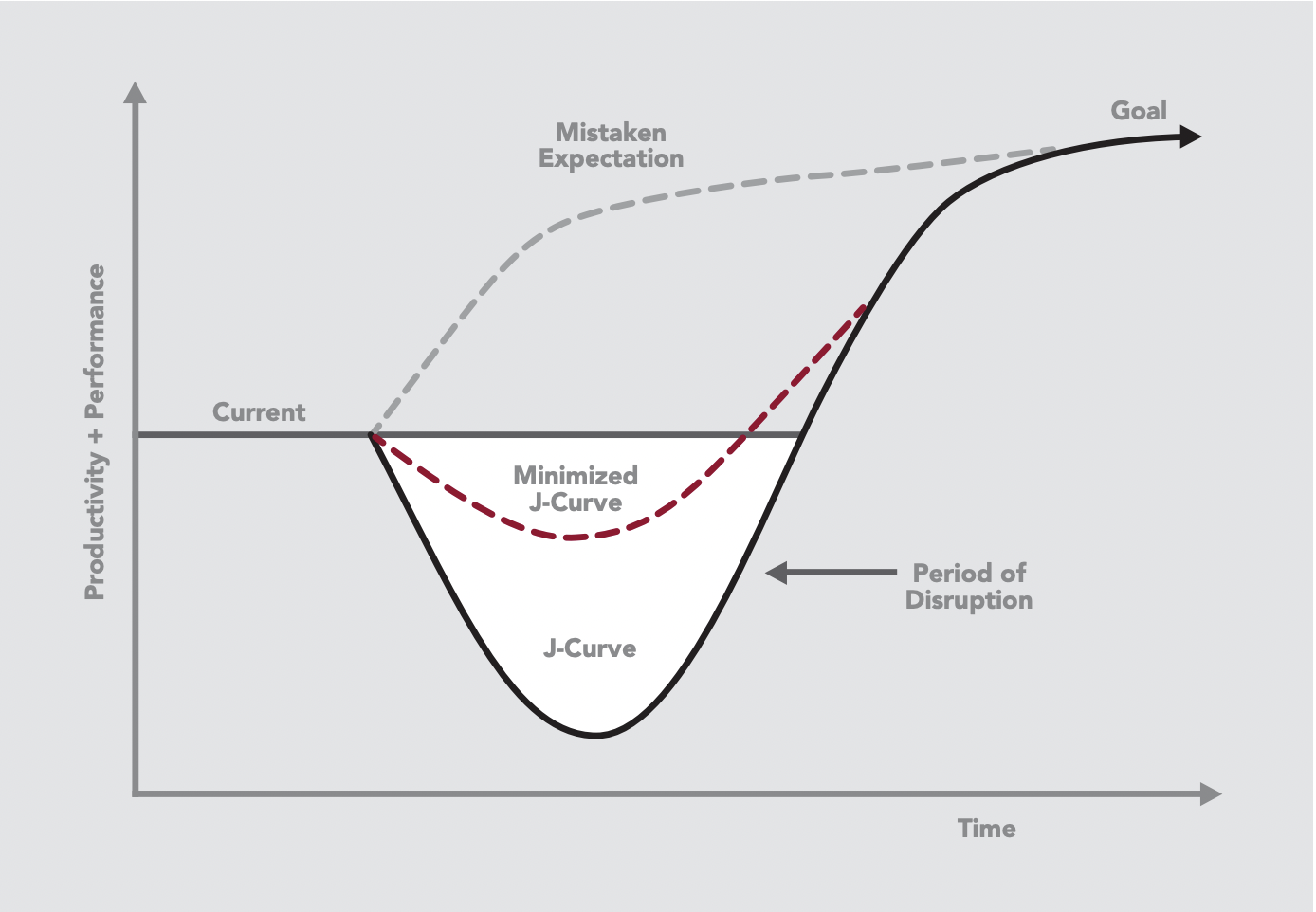

2. Understanding the AI J-Curve

The "AI J-curve" describes how returns evolve as companies adopt artificial intelligence: performance and productivity often decline initially, then recover and eventually rise sharply above the starting point.

Source: The AI adoption J-curve

#World Economic Forum. (2025). Four Futures for Jobs in the New Economy

Recent research from MIT Sloan examining U.S. manufacturing firms reveals a nuanced reality: AI introduction frequently leads to a measurable but temporary decline in performance, followed by stronger growth in output, revenue, and employment[1]. This J-curve trajectory helps explain why AI's economic impact has been underwhelming despite its transformative potential.

Recent empirical work on AI suggests the same dynamic. A 2025 study of AI investment, patents, and robot density found limited short-run productivity gains and explicitly linked the findings to an "AI Solow Paradox"[2]. The authors argue that AI's impact is consistent with a productivity J-curve: returns appear small or even negative in early years but are likely to accelerate as intangible capital accumulates. A 2026 literature review from BNP Paribas reaches a similar conclusion: AI can boost growth, but only if accompanied by significant investment in new capital, processes, and skills again describing AI as following a productivity "J-curve" with an initial latency period before aggregate benefits appear[3].

2.1 The Productivity Paradox

The research, titled "The Rise of Industrial AI in America: Microfoundations of the Productivity J-Curve(s)," analyzed data from U.S. Census Bureau surveys covering tens of thousands of manufacturing companies between 2017 and 2021[4].

The findings demonstrate that organizations adopting AI for business functions experienced a productivity drop of 1.33 percentage points in the short term. When correcting for selection bias, this negative impact was significantly larger approximately 60 percent larger than the baseline effect[4].

"AI isn't plug-and-play," explains Professor Kristina McElheran, a digital fellow at the MIT Initiative on the Digital Economy and lead author of the study. "It requires systemic change, and that process introduces friction, particularly for established firms."[5]

2.2 The Root Cause of the Dip

The initial productivity decline stems from a fundamental misalignment between new digital tools and legacy operational processes[6]. AI systems deployed for predictive maintenance, quality control, or demand forecasting require substantial complementary investments including:

- Data infrastructure modernization to support AI algorithms

- Comprehensive staff training programs to build AI literacy

- Workflow redesign to integrate AI capabilities seamlessly

Without these supporting elements in place, even the most advanced AI technologies can under deliver or create new operational bottlenecks[1]. The World Economic Forum identifies this "AI adoption J-curve" as being caused specifically by misalignment between digital tools and legacy processes regarding investments in data infrastructure, training, and workflow redesign[6].

3. Where the World Is on the AI J-Curve Today

3.1 The Reality of Value Generation

The gap between companies realizing substantial value from AI and those still experimenting is widening rapidly. According to BCG's 2025 "Build for the Future" report, only 5% of companies worldwide are generating substantial returns from AI at scale, while 60% are reaping minimal value despite significant investments[7].

The distribution of AI maturity reveals three distinct tiers:

- Future-built companies (5%): Generating substantial value and achieving five times the revenue increases and three times the cost reductions compared to other companies.

- Scaling companies (35%): Beginning to generate value as they expand AI initiatives.

- Laggards (60%): Reporting minimal revenue and cost gains despite substantial investment.

Research from McKinsey corroborates this challenge, revealing that for most organizations, AI use remains in pilot phases, and many companies have yet to scale the technology in ways that might offer tangible results[6]. A complementary study found that 95% of enterprise AI pilots fail to deliver measurable business impact[8].

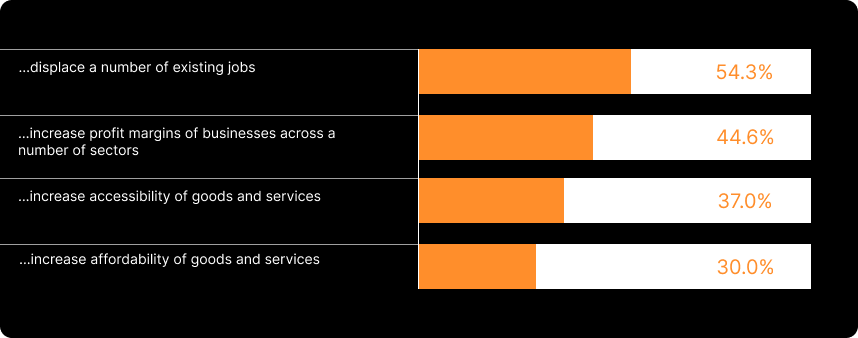

The World Economic Forum's recent AI and talent outlook notes that the share of businesses using AI in at least one function jumped from 55 percent in 2022 to 88 percent in the latest estimates an extraordinarily rapid diffusion of a frontier technology[9]. Executives overwhelmingly see AI as strategically important: about 45 percent expect it to increase profit margins, even as roughly 54 percent believe it will displace some existing jobs and 24 percent expect it to create new roles. This mix broad experimentation, high expectations, and anxiety about disruption is exactly what the J-curve framework would predict.

Source: World Economic Forum. (2025). Four Futures for Jobs in the New Economy

3.2 The Right Side of the J-Curve

If the present is characterized by friction and uneven benefits, the research consensus on the future is notably more optimistic.

McKinsey's estimates suggest that generative AI could increase the overall impact of artificial intelligence by 15-40 percent, pushing total AI-driven economic value into the tens of trillions of dollars by 2040[10]. That would make AI a growth engine on the scale of earlier general-purpose technologies like electrification or the internal combustion engine, especially important given demographic headwinds and slowing labor force growth in many economies.

BNP Paribas' review is more conservative on headline numbers, but converges on a similar qualitative view: AI may only produce incremental gains under business-as-usual, but can substantially lift long-run growth if accompanied by deep reorganization of production processes, capital renewal, and skills transformation[3]. That is precisely what the J-curve implies: the investment and reorganization happening now are the price of unlocking a higher, more sustainable productivity trajectory later.

State Street adds a more structural lens[11]. By dramatically lowering the marginal cost of generating, summarizing, and distributing knowledge work from drafting code to analyzing legal documents generative AI could accelerate the shift toward AI-augmented economies, compressing the timeline from investment dip to returns phase. They explicitly argue that the anticipated productivity J-curve "may be significantly shortened with generative AI" compared with past technology waves.

The implication is that the current turbulence is less a sign of over hyped technology and more a predictable phase in a transition that, if managed well, leads to a step-change in productivity and value creation.

4. The Manufacturing Adoption Landscape

Manufacturing has emerged as a leading sector in AI adoption, providing valuable insights into the J-curve phenomenon. As of 2025, over 52% of U.S. manufacturers have adopted AI at some level, representing a substantial increase from previous years[12]. More specifically, 77% of manufacturers have implemented AI to some extent, up from 70% in 2023[13].

AI deployment in manufacturing focuses primarily on:

- Production optimization (31%)

- Customer service enhancement (28%)

- Inventory management (28%)

- Supply chain management (49% of investment)

- Big data analytics (43% of investment)

The Deloitte 2025 Smart Manufacturing Survey provides compelling evidence of value realization for those who have navigated the J-curve successfully. Respondents implementing smart manufacturing initiatives reported, on average, a 10% to 20% improvement in production output, 7% to 20% improvement in employee productivity, and 10% to 15% in unlocked capacity[14].

5. Data Analytics: The Most Requested Capability

Although AI takes many forms, the consistently most in-demand capabilities at this stage are data and analytics. This is not a side story; it is the practical front line of the J-curve.

The World Economic Forum's Future of Jobs 2025 report finds that "analytical thinking" remains the single most sought-after core skill, with seven out of ten companies rating it as essential[9]. This emphasis reflects the critical role of data analytics in AI adoption success.

Organizations increasingly recognize that AI's value lies less in raw automation and more in generating actionable insights from large, complex datasets.

The AI and business intelligence adoption landscape for 2025 reveals significant momentum:

- 58.7% of organizations employ advanced business intelligence and analytics platforms

- 52.3% are standardizing and integrating data across departments

- 45.5% have established a corporate data strategy with enterprise-wide governance

- 20% enable employees to query data in natural language through AI-powered interfaces

Nearly one in four organizations expects to provide 30% or more of their workforce with direct access to AI-powered analytics within the next 12 months, signaling a democratization of data-driven insights[15].

6. Navigating the AI J-Curve: What Successful Organizations Do Differently

6.1 Digital Maturity as a Catalyst

Organizations that completed digital transformation prior to AI adoption experienced a significantly smoother transition. "Firms that have already done the digital transformation or were digital from the get-go have a much easier ride because past data can be a good predictor of future outcomes," Professor McElheran explains. "Once you solve those adjustment costs, if you can scale the benefits across more output, more markets, and more customers, you're going to get on the upswing of the J-curve a lot faster."[4]

6.2 The Scale Advantage

Company size plays a meaningful role in J-curve navigation. Larger organizations can distribute the substantial upfront costs of AI implementation including technology acquisition, infrastructure upgrades, and workforce training across broader revenue bases. Once these adjustment costs are addressed, larger firms can scale AI benefits across more output, markets, and customers, accelerating their ascent on the J-curve[4].

6.3 Treat AI as Organizational Transformation, Not a Point Solution

McKinsey's work on productivity J-curves emphasizes that technology alone rarely produces sustained gains. Firms that succeed couple AI deployment with process redesign, changes to operating models, and reskilling programs. Those investments deepen the initial dip but are what enable the later acceleration.

6.4 Invest Heavily in Data Foundations and Governance

The WEF's reports and numerous industry case studies converge on the same bottleneck: poor data quality and fragmented systems. Organizations that build robust data platforms, define clear ownership, and establish governance for data use move through the J-curve faster because each new AI use case can build on existing assets rather than start from scratch.

6.5 Prioritize Augmentation Over Wholesale Automation

Many productivity studies find that AI is most effective when it augments human capabilities improving decision quality, reducing drudgery, and freeing capacity rather than attempting to fully automate complex roles. This reduces organizational resistance, shortens learning cycles, and converts early gains into visible value rather than fear-driven pushback.

6.6 Align Talent Strategy with the Curve

Given the documented surge in demand for data and AI skills, organizations that move early to build or acquire analytical talent can better exploit the investment phase of the J-curve. Equally important is change management expertise: guiding teams through new workflows, metrics, and ways of working so that productivity dips are managed rather than allowed to spiral into failure.

7. The Promising Future

7.1 Long-Term Value

Despite initial setbacks, the MIT research demonstrates a clear pattern of recovery and eventual outperformance. Over a four-year period, manufacturing firms that adopted AI tended to outperform their non-adopting peers in both productivity and market share[4]. This recovery followed an initial adjustment period during which companies fine-tuned processes, scaled digital tools, and capitalized on the data generated by AI systems.

Early AI adopters are now demonstrating the transformative potential that justified their initial investments. Organizations that successfully navigated the J-curve are showing stronger long-term growth trajectories across multiple dimensions:

- Revenue increases driven by new AI-enabled products and services

- Cost reductions through optimized operations and predictive maintenance

- Market share gains from improved customer experiences and faster time-to-market

- Employment growth in higher-value roles requiring AI oversight and strategic decision-making

7.2 The Future-Built Advantage

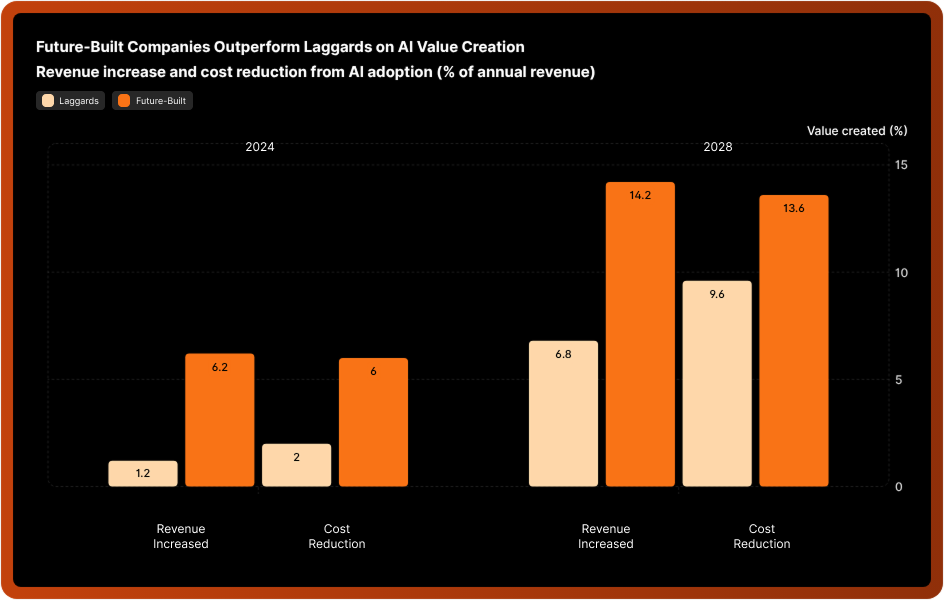

Future-built companies those 5% generating substantial AI value have established capabilities that create compounding returns. These organizations are reinvesting their AI gains into stronger technology and talent capabilities, creating a virtuous cycle of value creation[7]. These leading companies plan to spend 26% more on IT (representing almost a full percentage point of revenue) and dedicate up to 64% more of their IT budget to AI in 2025. As a result, they expect to see twice the revenue increase and 40% greater cost reductions by 2028 compared to laggards in areas where they apply AI[7].

Source: BCG Build for the Future 2025 Global Study

7.3 The Agentic AI Revolution

The emergence of agentic AI—autonomous systems that can plan, coordinate, and execute tasks across workflows represents the next frontier of value creation. AI agents already account for approximately 17% of total AI value in 2025 and are expected to reach 29% by 2028[7].

Future-built companies are leading this transition, allocating 15% of their AI budgets to agentic AI. A third of these organizations are currently deploying AI agents, compared with only 12% of companies scaling AI and virtually none among laggards[7]. Deloitte predicts that by 2025, 25% of enterprises using generative AI will launch agentic AI pilots, rising to 50% by 2027.

This shift from task automation to autonomous goal achievement represents a fundamental reimagining of how AI creates value. Rather than simply optimizing existing processes, agentic AI enables organizations to delegate complex, multi-step objectives to AI systems that can adapt their approach based on changing conditions and intermediate outcomes.

8. Conclusion: Patience as a Strategic Imperative

The AI J-curve reveals an uncomfortable truth for organizations accustomed to rapid technology returns: AI transformation requires patience, sustained investment, and fundamental organizational change. The initial productivity dip is not a signal to abandon AI initiatives but rather evidence that meaningful transformation is underway.

For the 60% of companies currently seeing minimal value from AI, the path forward requires systemic change across four dimensions:

- Data infrastructure modernization: Building robust platforms and governance to support AI at scale

- Workflow redesign: Integrating AI capabilities seamlessly into operational processes

- Capability building: Developing analytical talent and change management expertise

- Cultural adaptability: Fostering organizational willingness to experiment, learn, and iterate

The 5% of future-built companies already generating substantial AI value provide both inspiration and a roadmap. Their success demonstrates that the J-curve can be navigated successfully and that the long-term gains justify the short-term disruption. As these organizations pull further ahead, creating a widening value gap, the imperative for others to accelerate their AI maturity becomes increasingly urgent.

The most important insight from the J-curve phenomenon is this: AI's transformative potential is real, but realizing it requires organizations to match their technology investments with equally substantial investments in complementary organizational capabilities. Those willing to endure the dip and commit to fundamental transformation will emerge stronger, more competitive, and better positioned for an AI-driven future. Those who expect immediate returns or remain in perpetual pilot mode risk falling permanently behind.

As Professor McElheran notes, "Once firms work through the adjustment costs, they tend to experience stronger growth. But that initial dip the downward slope of the J-curve is very real."[4] The question facing every organization in 2026 is not whether to adopt AI, but whether they have the strategic patience and organizational commitment to navigate the J-curve successfully.

References

[1] MIT Sloan. (2025, June 30). The 'productivity paradox' of AI adoption in manufacturing firms. https://mitsloan.mit.edu/ideas-made-to-matter/productivity-paradox-ai-adoption-manufacturing-rms

[2] Scientific Research Publishing. (2025). AI investment and productivity: Evidence from the AI Slow Paradox. https://www.scirp.org/journal/paperinformation?paperid=146043

[3] BNP Paribas Economic Research. (2025, September 9). Productivity growth, employment and AI: A literature review. https://economic-research.bnpparibas.com/html/en-US/Productivity-growth-employment-AI-literature-review-9/9/2025,51822

[4] U.S. Census Bureau. (2025). The Rise of Industrial AI in America: Microfoundations of the Productivity J-Curve(s). Working Paper CES-WP-25-27. https://www.census.gov/library/working-papers/2025/adrm/CES-WP-25-27.html

[5] MIT Sloan. (2025, June 30). The 'productivity paradox' of AI adoption in manufacturing firms. https://mitsloan.mit.edu/ideas-made-to-matter/productivity-paradox-ai-adoption-manufacturing-firms

[6] World Economic Forum. (2025, December 29). AI paradoxes: Why AI's future isn't straightforward. https://www.weforum.org/stories/2025/12/ai-paradoxes-in-2026/

[7] Boston Consulting Group. (2025, October 15). Are You Generating Value from AI? The Widening Gap. https://www.bcg.com/publications/2025/are-you-generating-value-from-ai-the-widening-gap

[8] KORE.AI. (2026, January 11). The AI productivity paradox: Why employees are moving faster than enterprises. https://www.kore.ai/ai-insights/ai-productivity-paradox

[9] World Economic Forum. (2025). Four Futures for Jobs in the New Economy: AI and Talent in 2030. https://reports.weforum.org/docs/WEF_Four_Futures_for_Jobs_in_the_New_Economy_AI_and_Talent_in_2030_2025.pdf

[10] McKinsey & Company. (2023). The economic potential of generative AI: The next productivity frontier. https://www.mckinsey.com/capabilities/tech-and-ai/our-insights/the-economic-potential-of-generative-ai-the-next-productivity-frontier

[11] State Street. (2024). Assessing the economic impact of generative AI: Translating promise to reality. https://www.statestreet.com/web/insights/articles/documents/assessing-the-economic-impact-of-generative-ai-translating-promise-to-reality.pdf

[12] Xorbix Technologies. (2025, June 29). AI Adoption in the U.S. Manufacturing 2025: Which Industries Are Ahead? https://xorbix.com/insights/ai-adoption-in-the-u-s-manufacturing-2025-which-industries-are-ahead/

[13] Coherent Solutions. (2023, December 11). 2025 AI Adoption Across Industries: Trends You Don't Want to Miss. https://www.coherentsolutions.com/blog/2025-ai-adoption-trends

[14] Deloitte. (2025). 2025 Smart Manufacturing Survey. https://www.deloitte.com/us/en/insights/industry/manufacturing-industrial-products/2025-smart-manufacturing-survey.html

[15] Strategy Software. (2024, December 17). 5 AI and BI adoption trends every leader must know in 2025. https://www.strategysoftware.com/blog/5-ai-and-bi-adoption-trends-every-leader-must-know-in-2025